Recommended

Managerial Economics (Chapter 8 - Theory and Estimation of Cost)

security analysis and investment management

Theory of Production

Financial Derivatives and Options

Chapter 3 theory of consumer behavior

PRODUCTION& PRODUCTION FUNCTION

Production theory

Chapter 8: Cost Analysis

Recommended

Managerial Economics (Chapter 8 - Theory and Estimation of Cost)

security analysis and investment management

Theory of Production

Financial Derivatives and Options

Chapter 3 theory of consumer behavior

PRODUCTION& PRODUCTION FUNCTION

Production theory

Chapter 8: Cost Analysis

options and their valuation

Perfect competition

perfect competition, monopoly, monopolistic and oligopoly

Investment & Portfolio Management Booklet

Cost of capital

Chapter 18-The Markets for the Factors of Production.pptx

Options

Costs, revenue and profit

Production in Managerial Economics

stackelberg model

Capital market services

Firms in Competitive Markets

Isoquant

Accelerator Theory of Investment

2. bond valuation_and_interest_rates

9 costs class

The market structure

Production Function

4. domar's growth model

Investment function

Cost theories mm-aagac

BF Symposium-session2-Shin-Slides

More Related Content

What's hot

options and their valuation

Perfect competition

perfect competition, monopoly, monopolistic and oligopoly

Investment & Portfolio Management Booklet

Cost of capital

Chapter 18-The Markets for the Factors of Production.pptx

Options

Costs, revenue and profit

Production in Managerial Economics

stackelberg model

Capital market services

Firms in Competitive Markets

Isoquant

Accelerator Theory of Investment

2. bond valuation_and_interest_rates

9 costs class

The market structure

Production Function

4. domar's growth model

Investment function

What's hot (20)

options and their valuation

Perfect competition

perfect competition, monopoly, monopolistic and oligopoly

Investment & Portfolio Management Booklet

Cost of capital

Chapter 18-The Markets for the Factors of Production.pptx

Options

Costs, revenue and profit

Production in Managerial Economics

stackelberg model

Capital market services

Firms in Competitive Markets

Isoquant

Accelerator Theory of Investment

2. bond valuation_and_interest_rates

9 costs class

The market structure

Production Function

4. domar's growth model

Investment function

Viewers also liked

Cost theories mm-aagac

BF Symposium-session2-Shin-Slides

Cost concepts

Topic cost

7.02 c -establish__maintain_creditt

Production And Cost In The Short Run

Management Accounting: An Overview

Financial Market Ppt Kakul Zaidi

Credit: Principles and Sources

Financial management

Understanding Credit PowerPoint

Short run cost theory

Financial management

Financial Market Intermediaries

Financial management 2

Financial intermediation

Cost Accounting

Chapter1 financial intermediary

marginal cost accounting

Consumer finance ppt

Viewers also liked (20)

Cost theories mm-aagac

BF Symposium-session2-Shin-Slides

Cost concepts

Topic cost

7.02 c -establish__maintain_creditt

Production And Cost In The Short Run

Management Accounting: An Overview

Financial Market Ppt Kakul Zaidi

Credit: Principles and Sources

Financial management

Understanding Credit PowerPoint

Short run cost theory

Financial management

Financial Market Intermediaries

Financial management 2

Financial intermediation

Cost Accounting

Chapter1 financial intermediary

marginal cost accounting

Consumer finance ppt

Similar to Theory and estimation of cost

1517 cost-theory and estimation of cost

Production theory

Econ606 chapter 09 2020

Be chap4 the production process and costs

Cost Theory and Estimation

Product And Cost

Malla, ma. luisa

12 theory of cost and estimation

bechap5aug2018-180908000221.pdf

managerial economics unit 3 prof dr Kanchan.pptx

Chapter 5 : The Production Process and Costs

F0dd9 cost

topic 4

Cost analysis

Chapter 5 the production process and costs

Short Run Costs

and Output Decisions

Short-Run Costs

and Output Decisions

BR1.ppt

Econ 281 Chapter06.ppt

Econ789 chapter009

Similar to Theory and estimation of cost (20)

1517 cost-theory and estimation of cost

Production theory

Econ606 chapter 09 2020

Be chap4 the production process and costs

Cost Theory and Estimation

Product And Cost

Malla, ma. luisa

12 theory of cost and estimation

bechap5aug2018-180908000221.pdf

managerial economics unit 3 prof dr Kanchan.pptx

Chapter 5 : The Production Process and Costs

F0dd9 cost

topic 4

Cost analysis

Chapter 5 the production process and costs

Short Run Costs

and Output Decisions

Short-Run Costs

and Output Decisions

BR1.ppt

Econ 281 Chapter06.ppt

Econ789 chapter009

Recently uploaded

Black magic specialist in Canada (Kala ilam specialist in UK) Bangali Amil ba...

Benefits & Risk Of Stock Loans

TriStar Gold- 05-13-2024 corporate presentation

Famous Kala Jadu, Kala ilam specialist in USA and Bangali Amil baba in Saudi ...

najoomi asli amil baba kala jadu expert rawalpindi bangladesh uk usa

Kala jadu specialist in USA (Kala ilam expert in france) Black magic expert i...

Retail sector trends for 2024 | European Business Review

Sonagachi % High Profile Call Girls in Kolkata Real photos of Female Escorts ...

Webinar on E-Invoicing for Fintech Belgium

Jual obat aborsi Jogja ( 085657271886 ) Cytote pil telat bulan penggugur kand...

劳伦森大学毕业证

APPLIED ECONOMICS Sept 9FGHFGHFHGFGHFHGFHGFH

No 1 Top Love marriage specialist baba ji amil baba kala ilam powerful vashik...

Q1 2024 Conference Call Presentation vF.pdf

Sealdah $ Cheap Call Girls In Kolkata ₹7.5k Pick Up & Drop With Cash Payment ...

uk-no 1 kala ilam expert specialist in uk and qatar kala ilam expert speciali...

GIFT City Overview India's Gateway to Global Finance

Significant AI Trends for the Financial Industry in 2024 and How to Utilize Them

Famous Kala Jadu, Black magic expert in Faisalabad and Kala ilam specialist i...

black magic removal amil baba in pakistan karachi islamabad america canada uk...

Recently uploaded (20)

Black magic specialist in Canada (Kala ilam specialist in UK) Bangali Amil ba...

Benefits & Risk Of Stock Loans

TriStar Gold- 05-13-2024 corporate presentation

Famous Kala Jadu, Kala ilam specialist in USA and Bangali Amil baba in Saudi ...

najoomi asli amil baba kala jadu expert rawalpindi bangladesh uk usa

Kala jadu specialist in USA (Kala ilam expert in france) Black magic expert i...

Retail sector trends for 2024 | European Business Review

Sonagachi % High Profile Call Girls in Kolkata Real photos of Female Escorts ...

Webinar on E-Invoicing for Fintech Belgium

Jual obat aborsi Jogja ( 085657271886 ) Cytote pil telat bulan penggugur kand...

劳伦森大学毕业证

APPLIED ECONOMICS Sept 9FGHFGHFHGFGHFHGFHGFH

No 1 Top Love marriage specialist baba ji amil baba kala ilam powerful vashik...

Q1 2024 Conference Call Presentation vF.pdf

Sealdah $ Cheap Call Girls In Kolkata ₹7.5k Pick Up & Drop With Cash Payment ...

uk-no 1 kala ilam expert specialist in uk and qatar kala ilam expert speciali...

GIFT City Overview India's Gateway to Global Finance

Significant AI Trends for the Financial Industry in 2024 and How to Utilize Them

Famous Kala Jadu, Black magic expert in Faisalabad and Kala ilam specialist i...

black magic removal amil baba in pakistan karachi islamabad america canada uk...

Theory and estimation of cost

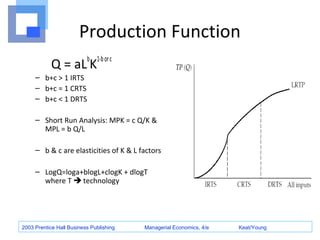

- 1. Production Function Q = aLbK1-b or c – b+c > 1 IRTS – b+c = 1 CRTS – b+c < 1 DRTS – Short Run Analysis: MPK = c Q/K & MPL = b Q/L – b & c are elasticities of K & L factors – LogQ=loga+blogL+clogK + dlogT where T technology 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 2. The Theory and Estimation of Cost • Definition of Cost • The Short Run Relationship Between Production and Cost – The Short Run Cost Function • The Long Run Relationship Between Production and Cost – The Long Run Cost Function • The Learning Curve 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 3. Definition of Cost • A cost is relevant if it is affected by a management decision. – Historical cost is incurred at the time of procurement – Replacement cost is necessary to replace inventory • Are historical costs relevant? 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 4. Definition of Cost • There are two types of cost associated with economic analysis – Opportunity cost is the value that is forgone in choosing one activity over the next best alternative – Out-of-pocket cost is actual transfer of value that occur • Which cost is relevant? 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 5. Definition of Cost • There are two types of cost associated with time – Incremental cost varies with the range of options available in the decision making process. – Sunk cost does not vary with decision options. • Is sunk cost relevant? 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 6. SR Relationship Between Production and Cost • A firm’s cost structure is related to its production process. – Costs are determined by the production technology and input prices. • Assuming that the firm is a “price taker” in the input market. 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 7. SR Relationship Between Production and Cost • Total variable cost (TVC) is associated with the variable input – Assume w=$500 per unit (price-taker) Total Input (L) Q (TP) MP TVC (wL) 0 0 0 1 1,000 1,000 500 2 3,000 2,000 1,000 3 6,000 3,000 1,500 4 8,000 2,000 2,000 5 9,000 1,000 2,500 6 9,500 500 3,000 7 9,850 350 3,500 8 10,000 150 4,000 9 9,850 -150 4,500 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 8. SR Relationship Between Production and Cost • TP and TVC are mirror images of each other Kings Dominion Example 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 9. SR Relationship Between Production and Cost • Total cost (TC) is the cost associated with all of the inputs. It is the sum of TVC and TFC. – TC=TFC+TVC • Marginal Costs • Average Costs Tool Set for Production Cost Analysis vs. Production Process Analysis 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 10. SR Relationship Between Production and Cost • Marginal cost (MC) is the change in total cost associated a change in output. MC TC Q = D D TVC TFC TFC TVC MC TC = D ( ) 0 = + D + D = D = D + 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young TVC Q Q Q Q Q D D D D D

- 11. SR Relationship Between Production and Cost • Add marginal cost to the table Total Input (L) Q MP TVC (wL) MC 0 0 0 1 1,000 1,000 500 0.50 2 3,000 2,000 1,000 0.25 3 6,000 3,000 1,500 0.17 4 8,000 2,000 2,000 0.25 5 9,000 1,000 2,500 0.50 6 9,500 500 3,000 1.00 7 9,850 350 3,500 1.43 8 10,000 150 4,000 3.33 9 9,850 -150 4,500 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 12. SR Relationship Between Production and Cost • Observe that: – When MP is increasing, MC is decreasing. – When MP is decreasing, MC is increasing. Total Input (L) Q MP TVC (wL) MC 0 0 0 1 1,000 1,000 500 0.50 2 3,000 2,000 1,000 0.25 3 6,000 3,000 1,500 0.17 4 8,000 2,000 2,000 0.25 5 9,000 1,000 2,500 0.50 6 9,500 500 3,000 1.00 7 9,850 350 3,500 1.43 8 10,000 150 4,000 3.33 9 9,850 -150 4,500 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 13. SR Relationship Between Production and Cost • The relationship between MP and MC is MP MC = D TVC = w ·D L = w · D L = · 1 = 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young w MP w Q Q Q D D D Law of diminishing returns implies that MC will eventually increase! Why?

- 14. The Short Run Cost Function • Average total cost (ATC) is the average per-unit cost of using all of the firm’s inputs (TC/Q) – Average variable cost (AVC) is the average per-unit cost of using the firm’s variable inputs (TVC/Q) – Average fixed cost (AFC) is the average per-unit cost of using the firm’s fixed inputs (TFC/Q) 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 15. The Short Run Cost Function • Add ATC = AFC + AVC to the table 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 16. The Short Run Cost Function • ATC = AFC + AVC 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 17. The Short Run Cost Function • Production cost graph or map is 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 18. The Short Run Cost Function • Important Map Observations – AFC declines steadily over the range of production. Why? – In general, ATC is u-shaped. Why? – MC intersects the minimum point (q*) on ATC. Why? 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 19. The Short Run Cost Function • Important Map Observations – What is the economic significance of q*? 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 20. The Short Run Cost Function • Average total cost (ATC) is the average per-unit cost of using all of the firm’s inputs (TC/Q) –At Q* - ATC is minimized or inputs are used most efficiently given the production function Going at 55 MPH 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 21. The Short Run Cost Function • A change in input prices will shift the cost curves. – If fixed input costs are reduced then ATC will shift downward. AVC and MC will remain unaffected. Computer Chip Case 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 22. The Short Run Cost Function • A change in input prices will shift the cost curves. – If variable input costs are reduced then MC, AVC, and AC will all shift downward. Airline Industry Case 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 23. The Short Run Cost Function • Yahoo Group Discussion – What is different about dot.com businesses? Irrational Exuberance 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 24. The LR Relationship Between Production and Cost • In the long run, all inputs are variable. – What makes up LRAC? 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 25. The Long-Run Cost Function • LRAC is made up for SRACs – SRAC curves represent various plant sizes – Once a plant size is chosen, per-unit production costs are found by moving along that particular SRAC curve 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 26. The Long-Run Cost Function • The LRAC is the lower envelope of all of the SRAC curves. – Minimum efficient scale is the lowest output level for which LRAC is minimized Is LRAC a function of market size? What are implications? 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 27. The Long-Run Cost Function • Reasons for Economies of Scale… Increasing returns to scale Specialization in the use of labor and capital • Economies in maintaining inventory • Discounts from bulk purchases • Lower cost of raising capital funds • Spreading promotional and R&D costs Management efficiencies 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 28. The Long-Run Cost Function • Reasons for Diseconomies of Scale… Decreasing returns to scale Input market imperfections Management coordination and control problems 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 29. The Learning Curve • Measures the percentage decrease in additional labor cost each time output doubles. – An “80 percent” learning curve implies that the labor costs associated with the incremental output will decrease to 80% of their previous level. 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young

- 30. The Learning Curve • A downward slope in the learning curve indicates the presence of the learning curve effect – Why? Workers improve their productivity with practice • The learning curve effect shifts the SRAC downward 2003 Prentice Hall Business Publishing Managerial Economics, 4/e Keat/Young